Drug manufacturers faced various types of obstacles in 2024. The healthcare system reforms, the European Union’s Joint Clinical Assessment (JCAS) preparation that went live at the end of January 2025, and drug shortage, with governments focus on cost control, are only a few. Among these challenges. In this review, Globaldata considers products that were factors affecting both approved and priced in 2024 and their launch strategy. The major trends that are considered include market priority, HTA assessment results, distribution of signals entering the market in 2024 and orphan drug design.

To understand the major launch trends in 2024, Globaldata reviewed a sample of new drugs, which was both approved and priced in 2024. Of the 33 drugs entering various markets in 2024, their launch sequence was reviewed to gain an understanding of the market priority.

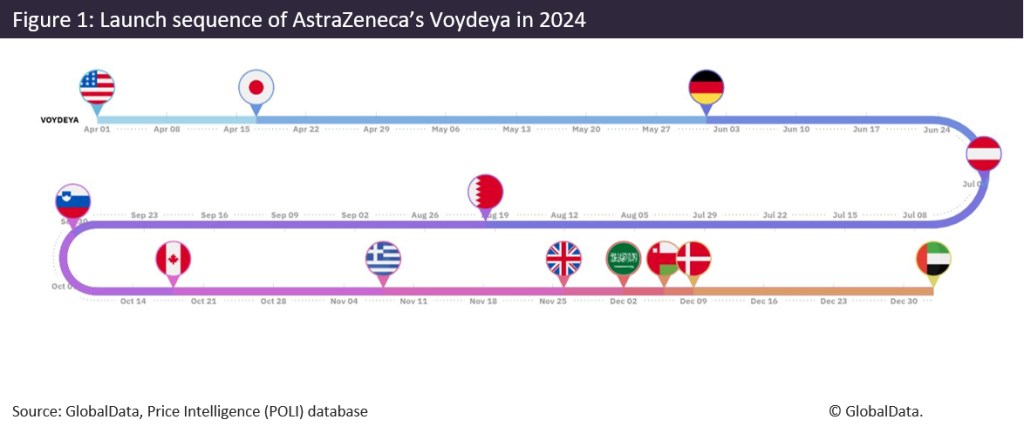

While the US remains an important first-launch market, APAC markets such as South Korea and Japan achieved the initial market for some products. For example, onconic theraputics (SK) Jacobo, on Cab, Q Zetas (Zastaprajan), Anti-Ularler Agent, which has been launched for the first time in South Korea in 2024 Korea, which may affect this launch strategy. . The drug has been launched in any other market so far. Similarly, Astrazeneca (UK) targeted an APAC market in 2024 as part of its launch strategy for Voydeya (Danicopan). While the brand was earlier launched in the US, its second market was Japan, followed by Germany. The full launch sequence for dannicopan is shown below.

The US traditionally has an initial launch market due to its free pricing policies and some price controls. However, last year, South Korea improved its reimbursement system to help develop a more supportive drug innovation environment. These policy amendments have affected the position of South Korea in the launch sequence. These changes included high early prices for innovative drugs, expansion of risk-sharing agreements, and improvement of drug reimbursement transparency. Similarly, Pharma welcomed several positive reforms in Japan in 2024, which potentially affects its position in the launch sequence. Many of these positive changes for branded drugs include: Extended eligibility criteria for price maintenance premium (PMP), price increase for unprofitable drugs, reducing the requirements of essential drugs, and significantly “pioneer premium” The beginning that is rewarded for treatment. In the first phase of its global rollout in Japan.

At the time of launch, the average price of Voydeya’s average price was evaluated to compare prices in all available markets and better understanding Japan and US prices for products. These were the first two markets where the product was launched, and despite the latch launched in Japan, the price of Voyedya’s per strength at the time of launch is in Japan ($ 0.25/Unit/mg) in the US ($ 0.23/units/mg) Was slightly more than. The average price per power unit at the time of launch was also the lowest in the US in all markets.

In the analysis of Globaldata of 2024 launch trends for selected drugs, the health technology assessment (HTAS) of each market was also considered. For those drugs that were approved in 2024 and were priced, there were a total of 16 decisions in seven markets. The figure below reflects the distribution of these results by the market. Both positive and neutral decisions represent drugs that are eligible for reimbursement. The decisions of a neutral result notes where products or indications are reimbursed to a restricted part of the population, or where the pricing process is not perfectly suited as a positive assessment. In Japan, UK, Canada, France and Germany, the drugs were evaluated, which was the leading to include all positive results either on resolution lists or more favorable pricing procedures. Most of the decisions distributed were in Japan. In Finland, after not being recommended for reimbursement, a negative result was provided for violey (zolbetuximab).

Review of these drugs by indication oncology reflects a continuous trend and significant investment in space, approved with most products (47%) and the price of falling within this medical field last year. This is followed by treatment for neurological disorders. Among the selected drugs that were launched in 2024 and were priced, 53% of brands had an orphan drug designation. While this ratio of orphan drugs reflects a continuous market trend of investing on high -cost featuring drugs for rare diseases, it may also indicate that orphan drugs may reach their peak. For example, price control and cost-control policies such as American Medicare Price Dialogue and recently increased treatment of diabetes such as rybelsus, wegovy, and ozempic (semaglutide) and mounjaro (tirzepatide) are possible danger for rare disease space .

While markets like America and Germany still maintain the initial launch market status, last year, a new market priority through specific pricing and reimbursement modification for developers as innovation from markets like South Korea and Japan. The paradigm may be trigger. While the US and Germany positions are unlikely to challenge globally, these markets have become more attractive to developers. In addition, as the rare disease place increases, it should be careful with the risks facing these drugs, including the current investment in diabetes and tightening government expenditure on high cost remedies in some important markets. . As the landscape develops and more products are launched in these markets, Globaldata will continue to follow these trends and whether they are distracted by the samples assessed in this review.

This article is produced as the world’s major resources, HTA and Market Access Intelligence for Globaladata’s Price Intelligence (POLI) service, global pharmaceutical pricing, which is widespread epidemiology, disease, clinical trials and globaldata The pharmaceutical intelligence center is integrated with manufacturing expertise. Our unique team of in-house experts monitors P&R policy development, results and data analytics worldwide, which gives an edge by providing important initial warning signals and insights to our customers. For a demo or more information, please contact us.